There are just too many moving parts.

Looking in 32/1, investing with Hugo Engels.

Introduction:

Happy new year, I think I can still say that, right? Good to have you back. As of late I have found myself in a rather indecisive mood. Well, when it comes to markets anyway. It feels like thinks are just moving around trying to find a new balance in the onset of 2025. Normally my base case is to mostly fade political developments in relation to markets. But this time I have a hard time trying to be unmoved by all the things I hear and read. It feels society has been beaten dull by the endless barrage of politicalizes opinions and narratives. It feels anyone can make up their own truth and just spew it into the world, totally adherent and absent of any responsibilities or consequences.

In the dead center of this new political world we find the upcoming US president, Donald Trump. Before he even started the job, he has made so many bold and (sometimes) unhitched statements, you really start to wonder if this is just his fetish or does he really means these things. Like buying Greenland…… I mean, really.

Now, don’t worry this is by no means a political blog. What I’m getting too, I see things move around a lot, with contradicting actions and reactions. Like, why does the oil price go up if many countries economies are struggling, oil producers are warning for declining sales, and we have a new president (elect) moving into the White house who wants to add more supply. Drill baby drill.

We have seen large abrupt moves in the equity market already for quite a while. Things rocket up or fall of a cliff on seemingly subtle news. Sentiment is based on short term developments. I’m happy with my portfolio, although I am reducing risk a tad bit, my aim is to be around 100 % invested.

Sometimes it’s just good to listen. I have the feeling that the US market and especially tech is considered expensive by market participants. But this has always been the case, this has made them scared to abandon their beloved growth stocks. Although market participants are also wondering.

When will the music stop?

10-years chart: QQQ (Nasdaq) Hist price, P/E

Anyone who has only a small interest in markets would have come across an indicator that shows us heading towards Dot.com bubble highs in valuation. Just to be clear we are still talking about US large and mega cap, especial in the tech space and the famous quality names. But what is the alternative? Moreover, do you dare to step away from the winners and trade them for the proverbial losers….? This dilemma has made the market edgy, especially if you consider second and third order effect. Short term price moves are decided by the masses. Participants are more worried about what other people will do than what they feel is fundamentally through. We have seen a somewhat small rotation away from the Mag7. But this is way early to call a secular trend. Sometimes you hear valuations don’t matter anymore, could be, this does infer the question:

If the market doesn’t care about valuations anymore, why would it start caring now?

There are a few key aspects to consider:

The US and yes also Europe is depended on a preforming stock market, our total pension system is reliant on market returns. Differently put, a rising US stock market is in the interest of governments around the world, especially for those with its constituent’s personal wealth linked to these assets (the voters|). This would surely motivate governments like the US, UK and EU to have policies insuring a rising market. Off course a rising market is not totally in their control, and they also have competing priorities. Still, I feel it is something to always consider when looking at markets.

Next tot that, high valuations are not a sure trigger for a reevaluation cycle or a crash. Things can be expensive in relation to history for indefinitely. Moreover, they can become even more expensive.

Markets can stay irrational way longer that you can stay solvent.

Yes, we know………

Still, there is truth in this, although the overpriced argument does hit home with me, I feel a above average chance for a market crash is still small. Or better said, slightly elevated. It is my base case markets will continue being choppy. Sure, some small bubbles can be popped, just as they make room for new ones. Moreover, I expect a flat market for 2025 with value and Ex US stocks catching up slightly instead of US stocks ‘catching down’.

Having a large income creating asset allocation should favor this scenario. With off course overweight in EU & UK. Yes, I know this sounds like talking my book and I realize a small catching up will not compensate for the underperformance of 2024 & 2023.

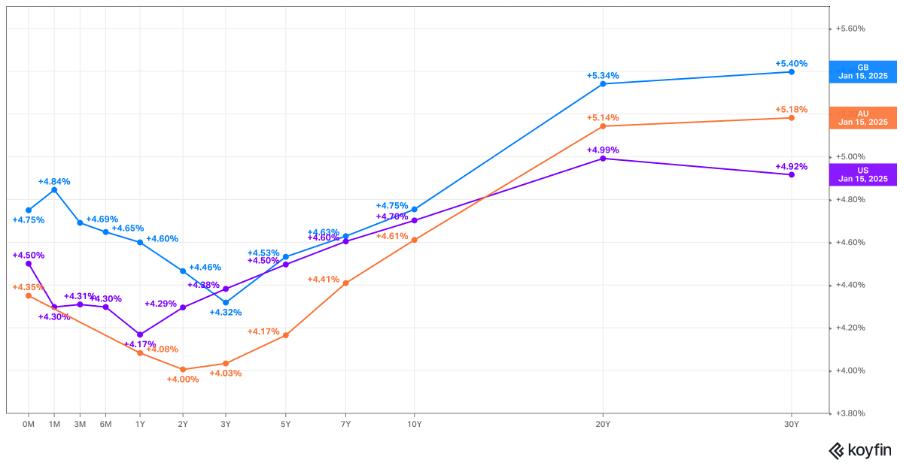

This brings me to another thing I’m wrestling with. Fixed income. EU rates are again moving to territories that are not compelling to allocate to. I feel when it comes to EU, equities are the best choice. When we look beyond the EU, and this means for me, taking currencies risk, the US long-end does look tempting, only I feel the dollar is too strong. At the moment I like UK and Australian fixed income. In both cases I like owning the hole yield curve.

Yield curve UK (GB), Australia (AU), US

I am wondering if the short end is still more interesting compared to the 20 to 30-years considering duration. The same feeling I have with corporate credit. Less than 1 % in yield (Opt, Adj.) spread is just not a reasonable compensation for the difference in risk. Same can be sad for high yield.

3-years chart: Opt. Adj. yield high grade broad

BDCs (Business Development Companies) have also been something that can be reaching the top of the cycle; they had a big tailwind with the rising yield environment and was one of my better investments in the 2022 to 2025 era. This because most of the loans they give out are floating rate and defaults where modest. Now, that rates are coming down slowly the spreads they earn can reduce somewhat. Moreover, there success has drawn a lot of capital, this can create overcrowding. With subsequently deteriorating deal quality. On the other hand, these lower yields can also be beneficial for their customers. This can reduce the chance for defaulting. What I am looking at is the book value of these BDC, if they start trading around 1 times book value I am tempted to reallocate.

So, to wrap this up.

My apologies, a wait and see attitude is the best I can come up with. There are just too many moving parts. I’m happy with the portfolio I hold. I would not be surprised that it could have a good year relative to the broader market. Moreover, some alleviated volatility is reasonable to expect and I’m in a good position to take advantage. I’m a fundamentally driven investor, I look for quality businesses that are undervalued relative to their intrinsic value. I look beyond the big names in mostly the small and mid-Cap markets. Investing is a skill that combines knowledge and imagination. You need patience and control over your emotions. Whatever will happen, it will be fascinating to see. Do remember it’s only money and there are more important things in the world. That’s why I hope we will see more peace in the world and less hardship. We should all care more and hate less.

Let me end with this.

Slowing down sometimes feels like the only remedy against all the turmoil in the outside world and within the mind. Mastering this is the goal for 2025 and beyond.

About the letter:

Dear reader, I’ve decided to start a letter on my investing process. I’m not a professional trader or investor and I hold no licenses or registrations. This letter can never be viewed as investment advice and the expressions and opinions that are written are mainly for entertainment purposes only.

Through this letter I want to evolve my own investment process and maybe give the reader an interesting prospective of a retail trader who enjoys markets and investing. If you are a starting investor who wants to go beyond the passive index fund, buy and hold strategy and would like to construct a more personal portfolio based on fundamentals this could by a nice letter for you to follow. Of course, any other reader would be more than welcome, and I would also love to have feedback. This is first of all a learning process for me.

In this letter I want to give my personal view on markets and investment processes. It will be from a European perspective with a clear value orientated focus. With an extra focus on The Netherlands. Hope you enjoy,

Hugo Engels